Rovensa Next invited Carlos Cogo, a renowned agribusiness consultant, to share his analysis and perspective on the Brazilian market today. Discover his insights and recommendations:

By Carlos Cogo | Agribusiness Consultant | COGO Agribusiness Intelligence

Brazilian agribusiness is undergoing a quiet but consequential inflection point. Against a backdrop of compressed margins, tightening credit, elevated interest rates, and persistent geopolitical volatility, biological inputs have transitioned from a sustainability narrative into a financial decision. Producers adopting biologicals today are not merely responding to environmental imperatives — they are managing their cost structure.

From Niche to Scale: A Market in Structural Expansion

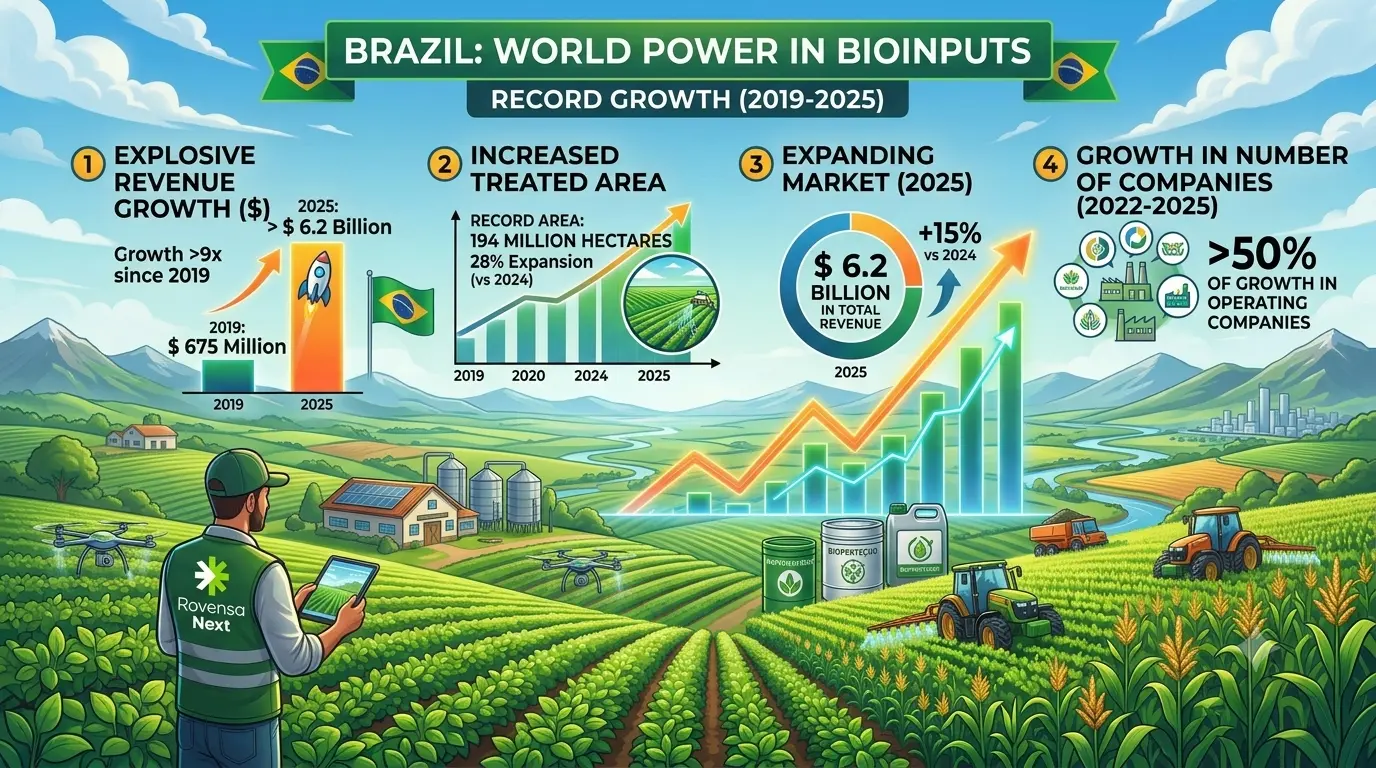

Brazil has consolidated its position as one of the world’s largest producers and consumers of biological inputs. In 2025, the bioinput market surpassed BRL 6.2 billion in total revenue — a 15% increase over the prior year — while treated area reached a record 194 million hectares, expanding 28% over 2024. The sector has grown more than ninefold in revenue since 2019, when it stood at BRL 675 million. Between 2022 and 2025, the number of companies operating in the segment grew by more than 50%.

Within the sector, bionematicides recorded the most significant area expansion in 2025, adding 16 million hectares — a 60% increase over 2024 — and cementing their role in mainstream integrated pest management protocols. By revenue, bioinsecticides led at 35% of total market value, followed by bionematicides at 30%, biofungicides at 22%, and inoculants at 13%. Inoculants were applied across 77 million hectares, reflecting their central role in Brazil’s transition toward lower-emission agriculture.

Brazil now represents 18% of the global bioinputs market and accounts for half of all financial flows in the segment across Latin America. By the end of the decade, the sector is projected to expand by 66% in treated area, with revenue forecast to reach BRL 9.88 billion by the 2029/30 crop season. These are not aspirational figures — they are grounded in already-documented adoption rates and regulatory momentum.

The Economic Equation That Changed the Calculus

The underlying rationale is straightforward. In 2025, Brazil imported a record 43.3 million metric tons of fertilizers, with total fertilizer deliveries to the domestic market reaching 49 million metric tons — also a record — according to the National Association for the Diffusion of Fertilizers (ANDA). Brazil is the world’s largest fertilizer importer, accounting for 23% of global imports, with a total import bill of USD 16.73 billion in 2025.

Import dependency by nutrient has intensified. In 2025, Brazil imported 88% of its total fertilizer consumption, 96% of its potassium, 95% of its nitrogen, and 72% of its phosphorus. Domestic production remained effectively flat at approximately 7.2 million metric tons — far below the pace required to close the structural gap. Fertilizers represent, on average, 23% of total production costs for soybeans, maize, and cotton, making supply disruptions a direct threat to farm-level profitability.

The geopolitical concentration of this dependency amplifies the structural risk. Russia remained Brazil’s largest fertilizer supplier in 2025, accounting for 28.2% of total import volume in the first half of the year — and an estimated USD 4.36 billion in annual import value — supplying critical volumes across all three primary macronutrients. Approximately 45% of Brazil’s fertilizer imports originate from countries classified as geopolitically unstable, placing the country among the most exposed agricultural economies globally.

The closure of the Strait of Hormuz following the Iran conflict that began in late February 2026 has transformed this vulnerability from a theoretical risk into an acute operational crisis. Under normal conditions, approximately one-third of global seaborne fertilizer trade transits the strait. With traffic effectively halted, urea prices surged over 30% within a single week, nearly one million metric tons of fertilizer cargo became physically stranded in the Gulf, and major producers declared force majeure. The FAO has warned of a potential global agri-food catastrophe, with harvest impacts extending into the second half of 2026 and through 2027.

Biological inputs offer a domestically anchored solution to a globally sourced problem. Approximately 85% of bioinput production used in Brazilian fields is manufactured by companies based in the country, effectively eliminating currency exposure and decoupling producers from intercontinental supply chains. As practitioners in the sector observe, biological products are inherently incompatible with long-haul logistics — they must be produced close to the point of application.

The agronomic efficiency argument is equally compelling. In the case of phosphorus, only 30% of applied nutrients are absorbed by crops — the remaining 70% are lost to soil fixation. The deployment of phosphate-solubilizing microorganisms to improve this efficiency by even 10 percentage points translates into a measurable reduction in input cost and import dependency at national scale. Economic analyses indicate potential annual savings of up to USD 5.1 billion by integrating microbial inoculants into nutrient management programs in key cereal and energy crops.

Structural Headwinds: Margins, Commoditization, and the Path to Differentiation

Despite robust area-based growth, the revenue trajectory of the bioinput sector reflects a more nuanced picture. After two consecutive crop cycles of effective stagnation in revenue — driven by declining average selling prices and accelerated commoditization — the market recovered strongly in 2025, with total revenue rising 15% to BRL 6.2 billion. Nevertheless, structural tensions persist.

More than 150 companies are currently competing in a market that demands minimum operating margins of 15% to 20% for commercial viability — a threshold that renders sustained R&D investment economically unviable for most. The margin range necessary to support meaningful innovation is estimated at 30% to 50%. With the benchmark interest rate at 15%, the opportunity cost of capital effectively competes with sector returns. Producers exercise strong bargaining power in a fragmented supply landscape: when two comparable products are available, the lower-priced option wins. The result is a commoditization dynamic that penalizes innovation and compresses margins across the value chain.

The path forward lies in differentiation. The players that will lead the next phase of sector consolidation are those combining scale, registered product portfolios, and demonstrated technical performance at field level. This dynamic is already accelerating M&A activity and the exit of undercapitalized operators from the market.

Regulatory Reform: The Next Structural Catalyst

The Brazilian National Bioinputs Law (Law No. 15,070/2024), enacted on December 23, 2024, establishes a comprehensive regulatory framework for biological inputs across agricultural, livestock, aquaculture, and forestry systems. The legislation formally recognizes that a single microorganism may perform multiple agronomic functions — a distinction that previously exposed manufacturers to registration penalties and procedural bottlenecks. The framework also creates a pathway for co-formulation currently authorized only for seed treatment applications.

The regulatory momentum is already visible in market outcomes: Brazil registered 162 newly approved bioinput products in 2025 — the highest annual total on record. The National Bioinput Program (PNB), established under Decree No. 10,375/2020, coordinates government agencies, the private sector, academic institutions, and civil society around eight strategic objectives — spanning regulatory policy, rural credit, research infrastructure, and smallholder agriculture. Complementary measures under development are expected to enable combined fungal-bacterial formulations — currently operating in a legal grey zone — and to further reduce registration timelines.

Brazil’s Competitive Advantage: Underutilized but Substantial

Brazil possesses a unique combination of attributes that position it to lead globally in biological inputs: unparalleled tropical biodiversity, a consolidated scientific base anchored by institutions such as ESALQ/USP and EMBRAPA, domestic production capacity, and a large-scale commercial farming system that already validates and deploys these technologies at field scale. The number of registered companies producing inoculants alone rose from 36 in 2021 to 63 in 2025.

The development cycle for new biological products is materially faster and less capital-intensive than for conventional chemical crop protection — averaging two to five years at a cost of BRL 1 million to BRL 2 million, roughly half the timeline and 10% of the cost of a synthetic chemical equivalent. Inoculants can reach the market within 18 months. Use of bioinputs generates estimated annual savings of approximately BRL 165 billion for the Brazilian economy — a figure that underscores the macroeconomic relevance of scaling adoption well beyond the farm gate.

The Producer as the Driving Force of the Transition

At the center of this transformation is the Brazilian producer operating under tighter profitability constraints and shorter credit horizons. It is precisely this environment of financial pressure that has accelerated the adoption of biologicals as a cost management strategy — not as an ancillary sustainability initiative. In 2025, biocontrol adoption surpassed 43% of the 85 million hectares planted with the principal commodity crops, with soybeans and maize accounting for 77% of total bioinput use.

The partial substitution of chemical applications with biological solutions across key commodity crops — including soybeans, maize, cotton, and sugarcane — is an expanding and irreversible reality. Producers are exercising greater selectivity, applying more rigorous cost-benefit analysis per cultivated hectare. Biological inputs have consistently demonstrated their value within that framework.

Brazil did not arrive at its leadership position by coincidence. It is the result of converging economic pressure, scientific capacity, and productive scale. The structural dependency on imported fertilizers — now acutely exposed by the Strait of Hormuz crisis — makes the domestic bioinput industry not merely a competitive advantage, but a strategic national imperative. The next critical step is converting market leadership into sustained commercial performance: through functional regulation, margins that support innovation, and clear strategic positioning for the players committed to growing with consistency in this sector.

By Rovensa Next:

Biosolutionize Agriculture in Brazil, Integrated biosolutions strategies driving efficiency, profitability and sustainable crop performance

Based on the market dynamics presented by the renowned agribusiness consultant Carlos Cogo, Rovensa Next addresses rising input costs, nutrient inefficiencies and increasing production risks through integrated biosolutions strategies focused not on applying more inputs, but on using them more efficiently.

While Brazil remains highly dependent on imported fertilizers, Rovensa Next offers a differentiated and strategic advantage through biosolutions developed, produced and scaled locally. Solutions such as Atmo, a biofertilizer that promotes biological nitrogen fixation in legumes, Azzofix, a biofertilizer based on Azospirillum brasilense to promote biological nitrogen fixation, and Phós’Up, which solubilizes insoluble phosphates and helps plants to better utilize phosphorus, help increase nutrient availability by 10–30%, according to Rovensa Next trials, promoting more efficient use of these nutrients and optimizing productivity and production quality. Solutions such as Otimais Duo support biological nitrogen fixation, phosphorus availability and improved nutrient use efficiency, maximizing the return on fertilizer investments. The dual-microbial technology offered by Otimais Duo has been validated in 94 field trials across seven countries and ten crops1, with maize trials showing an average yield increase of 1,302 kg/ha, while soybeans have reported average gains of 600 kg/ha, according to Rovensa Next trials.

These programs are complemented by biocontrol solutions such as Prev-Am, which provides insecticidal, acaricidal and fungicidal activity through our patented Orowet® technology, as well as Row-Vispo and Milarum, our advanced biofungicides based on Bacillus subtilis that help growers manage disease pressure, diversify modes of action and support resistance management while reducing dependence on conventional crop protection tools. In addition, Row-Vispo combines the Bacillus subtilis IAB/BS 03 isolate with BIOEVOLOGY® formulation technology to support high-performance foliar disease control.

Wetcit Gold further optimizes field performance by enhancing spray coverage, wetting, spreading and penetration, thereby improving the efficiency of crop protection and nutrition applications.

Rovensa Next’s approach to the fertilizer crisis is built on a simple but transformative principle: efficiency through integration rather than substitution. Rather than replacing conventional fertilizers with a single alternative, we offer a combination of complementary biosolutions that are designed to support nutrient availability and uptake and help crops perform more efficiently during the key stages of the crop cycle.

This integrated strategy addresses two of the core challenges behind today’s fertilizer crisis — price volatility and supply uncertainty — and it helps growers obtain more value from every unit of nutrient applied. This is achieved by improving root performance, soil vitality, and soil nutrient dynamics; enhancing natural nutrient cycling; and helping plants make better use of the nutrients that are already present in the soil.

This boosts plant metabolism and resilience, unlocking more efficient nutrient use and stronger crop performance even under stress conditions. By combining these levers, Rovensa Next enables growers to maintain performance while adopting more resilient and adaptive nutrition strategies to respond to increasing cost pressure and market volatility.

Backed by a global manufacturing and R&D network across Brazil, Mexico, the United States, Latin America, and Europe, Rovensa Next combines local production with global expertise, providing growers with greater supply security, innovation and long-term resilience. Brazil plays a key role in this strategy through its integrated innovation ecosystem, including the new pilot fermentation plant in Monte Mor and the Global Research and Innovation Center in Hortolândia, which accelerate the development of next-generation microbial biosolutions.

Together, these integrated biosolutions strategies help Brazilian growers maximize resources, protect yield and profitability, manage resistance more effectively, and build more resilient, sustainable production systems.

Carlos Cogo’s analysis sources:

- Cogo Agribusiness Intelligence

- ANDA (National Association for the Diffusion of Fertilizers)

- FAO

- Ministry of Agriculture and Livestock (MAPA)

- EMBRAPA

- National Bioinputs Program (PNB)

- Brazilian Bioinputs Law No. 15,070/2024

- Public market data and industry reports

Rovensa Next sources:

- 1 Otimais Duo R&D exploration and research 2023–2026 by Rovensa Next and external research companies.